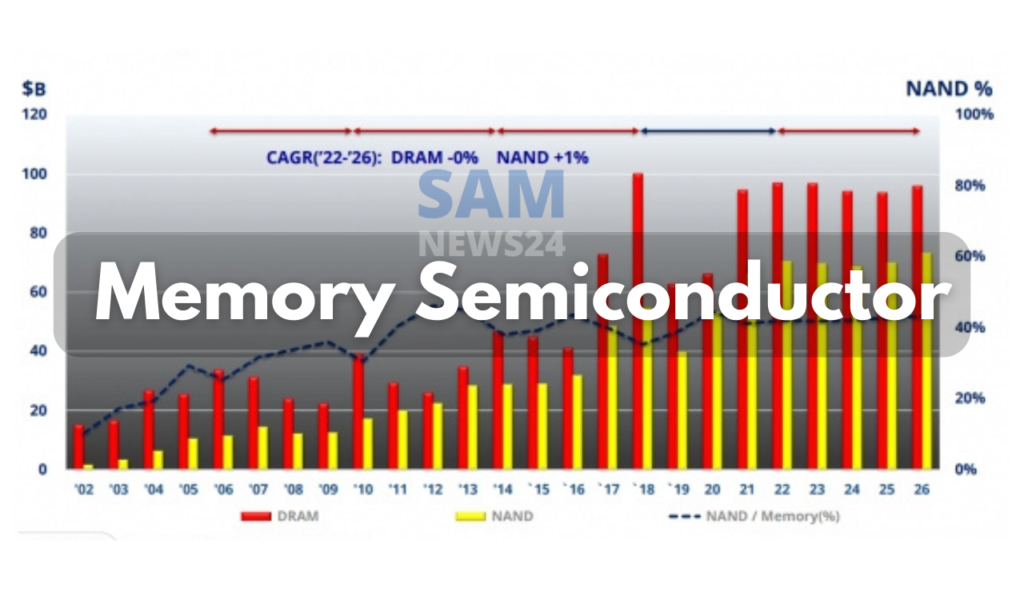

As we continuously tend to listen to the memory semiconductor market whose demand has been drastically reduced. This slow-down condition arises due to the global recession in the semiconductor market. The same condition we expected to face till 2025 and the rebound phase starts to begin in 2026.

Reportedly, recently organised a ‘SEMI Members’ Day 2022 event by the International Association of Semiconductor Equipment and Materials (SEMI) held at Suwon Convention Center. SEMI Members Day is a yearly event that discloses the updates on SEMI Korea and the global economy, semiconductor technology and market outlook.

Speakers of the event

Here the speaker of this event are SEMI President Cho Hyundai, Head of NH Investment Securities Kim Hwan, Vice President Kim Soo-Jung and Vice President of IDC, Choi Jeong-dong TechInsiders Fellow, Attorney Yul Chon of Chung Dae-won Law Firm, and Daniel Tracy Techcet Senior Director respectively.

On the day of the event, IDC Vice President Kim Soo said- While the semiconductor is expected to grow by 4.1% from 21 to 24 years. But in the case of memory semiconductors, the growth rate is expected to remain at 1%. All because the decline in the IT market includes PCs and smartphones. He also said that the same condition occurs and rebound happens until 2025.

DRAM and NAND demand expected to increase

Additionally, if talking specifically then both DRAM and NAND are forecasted to see a trend of recovering demand again next year. But before that, a more sluggish demand going to arise this year as compared to the initially expected. While the DRAM demand growth rate has been tending to reduce from the existing 17% to 10%. Whereas the NAND demand growth rate has been continuous lowering from the existing 30% to 19%. By that time, the demand curve from the next year is expected to rebound once and face a modest decline.

At the same time, prices are expected to rebound once in both DRAM and NAND and that starts to begin from Q3 next year. Although annually the downtrend continues, the market size remains to stagnate even if the demand increases.

“With the rapid increase in memory manufacturers’ reconciliation, DRAM and NAND prices will continue to fall by 10-20% per year,” explained IDC Vice President Kim Soo-chung, “Especially in the NAND market, where there are more major competitors than DRAM and this phenomenon will only intensify.”

To drive the event ahead by the Choi Jung-dong. He is the TechInsiders Fellow presented the latest technology trends as well as the future prospects for memory semiconductors.

“Previously, Samsung Electronics‘ DRAM cell scaling technology was ahead of other competitors (SK Hynix, Micron), but starting with the 1z (15nm class) DRAM in 2020, the technology of the three companies has reached virtually the same level,” said Choi Jung-dong, TechInsiders Fellow, “

And since the attempts to increase DRAM integration continue, 1c (11-12nm class) DRAM will be developed in 2025 and by 2029 tentatively. That makes us enable to enter into the era of single-digit nm DRAM classes.

Concerning the NAND, in which it is believed that the majority of the companies are involved in developing 400-500 units. While in the coming 8-9 years 800 stage lamination technology can be developed.